Key Takeaways: Secure financial document sharing requires encryption, access controls, audit trails, and automatic expiration. This article is for accountants, tax preparers, financial advisors, mortgage brokers, and wealth managers who handle sensitive client financial data.

Why Financial Documents Are Prime Targets

A single tax return contains full names, Social Security numbers, addresses, dates of birth, income details, bank account numbers, and investment holdings. A bank statement reveals account balances, transaction patterns, and merchant relationships. A loan file adds employment history, salary details, credit reports, and property appraisals. These documents are complete identity profiles that attackers can exploit for years.

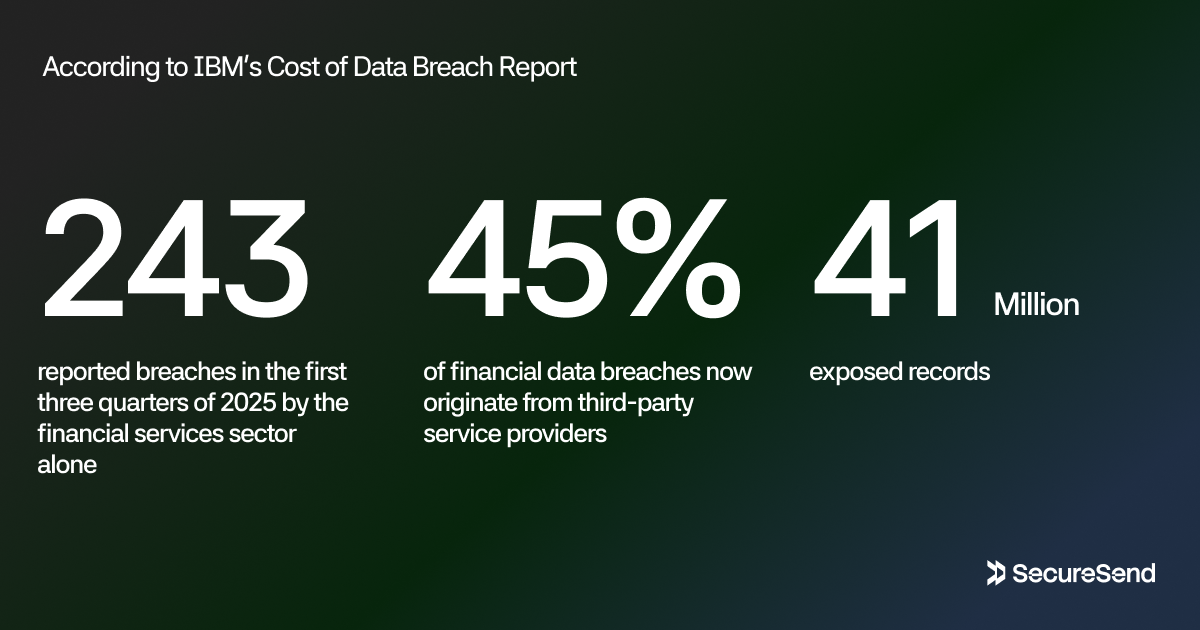

The statistics paint a clear picture. In 2025, an estimated 97% of all data breaches were financially motivated. Roughly 68% of those involved ransomware or extortion campaigns. The financial services sector alone saw 243 reported breaches in the first three quarters of 2025, exposing over 41 million records. IBM's Cost of Data Breach Report 2025 puts the average cost globally at around $4.44 million, with U.S. organizations facing an average of $10.22 million per incident.

Tax professionals face particularly intense targeting. The FBI's Internet Crime Complaint Center reports that tax firms are over four times more likely to experience targeted cyberattacks than general small businesses. A single compromised tax return provides everything needed to file fraudulent returns, open credit accounts, or commit synthetic identity fraud for years to come.

The threat is not limited to direct attacks on your office. Approximately 45% of financial data breaches now originate from third-party service providers. When you share client documents with a bookkeeper, a mortgage broker, an insurance agent, or a financial planner through insecure channels, you extend your attack surface to their systems and their security practices.

Financial professionals who still rely on email attachments and consumer cloud links are playing a dangerous game. The real question is whether your sharing practices can withstand an attack.

The Problem with Email Attachments and Consumer Cloud Tools

Email remains the default method for sharing financial documents. It is familiar, fast, and requires no additional training. But standard email was never designed for the sensitivity of financial data.

When you attach a tax return to an email, that document travels through multiple servers before reaching your recipient. While TLS encryption protects messages in transit between hops, the protection is temporary. Messages and attachments are often stored in plaintext on mail servers and end-user devices. Once delivered, the sender has no visibility into whether the document was opened, forwarded, downloaded, or copied. If the recipient's email account is compromised six months later, every attachment you ever sent them is now in the attacker's hands.

Consumer cloud tools like Google Drive, Dropbox, and WeTransfer create a different set of problems. These services encrypt files at rest and in transit, but they hold the decryption keys. Their employees can access your files. A hacker who breaches their infrastructure can too. A government agency with a subpoena can compel them to produce your data. The "anyone with the link" sharing model that makes these tools convenient also makes them dangerous. Links get forwarded to unintended recipients, copied into chat messages, and posted in places they should never appear. There is no expiration, no revocation, and no meaningful audit trail.

For tax professionals, the risks are compounded by regulatory obligations. The IRS Security Six framework mandates specific controls for all devices and systems containing taxpayer data. Email attachments and consumer cloud links violate multiple principles of this framework. They lack proper access controls. They do not provide adequate audit trails. They cannot enforce multi-factor authentication for recipients. And they offer no mechanism for secure disposal once the document has served its purpose.

The Gramm-Leach-Bliley Act's Safeguards Rule, as amended in 2021 and strengthened through 2024, now explicitly requires financial institutions to encrypt customer information both at rest and in transit, implement multi-factor authentication, maintain detailed audit trails, and securely dispose of customer information no later than two years after it is last used. Email attachments and open cloud links make compliance with these requirements nearly impossible.

You do not need to abandon digital sharing. Choose tools and practices designed specifically for the risks and regulations that financial professionals face.

What Regulators Now Require

Financial professionals operate under a dense web of overlapping regulations. Understanding the core requirements helps explain why secure document sharing has moved from optional to mandatory.

IRS Security Six for Tax Professionals

The IRS, in partnership with state tax agencies and industry partners, established the Security Six framework through IRS Publication 4557. All tax professionals must implement these six controls:

- Anti-virus and anti-malware software on all devices

- Firewall protection for network perimeters and individual devices

- Multi-factor authentication for all systems containing taxpayer data

- Automatic security updates for operating systems and software

- Data backup and recovery with verified restoration capability

- Drive encryption using AES-256 full-disk encryption on all devices

These requirements form the foundation, but they are not the complete picture. The IRS also mandates written information security plans, staff training on phishing and data theft recognition, and immediate reporting of suspected breaches to the IRS, FBI, and state authorities.

GLBA Safeguards Rule

The FTC's amended Safeguards Rule, effective June 2023 and further strengthened in 2024, applies to all financial institutions under GLBA jurisdiction. This includes tax preparers, accountants, financial advisors, mortgage brokers, and many other professionals who handle financial data. FTC Safeguards Rule (16 CFR Part 314) key requirements include:

- Written information security programs with risk assessments

- Encryption of customer information at rest and in transit

- Multi-factor authentication for access to information systems

- Access controls limiting users to the minimum necessary data

- Audit trails logging who accessed what, when, and from where

- Secure disposal of customer information within two years of last use

- Annual penetration testing and semi-annual vulnerability scans

- Incident response plans with 30-day FTC notification for breaches affecting 500+ consumers

Non-compliance carries serious penalties. The FTC can impose fines up to $100,000 per violation. Officers and directors can face personal fines up to $10,000 per violation and imprisonment up to five years.

PCI DSS for Payment Data

Professionals who handle payment card information must comply with PCI DSS requirements, including encryption of cardholder data, firewall protection, updated anti-virus, strong access controls, and physical security around systems storing card data.

State-Level Requirements

California's CCPA, New York's SHIELD Act, and an expanding patchwork of state breach notification laws impose additional obligations. Many states now require encryption as a safe harbor against breach notification requirements, meaning that if data is properly encrypted and the encryption key is not compromised, the breach may not trigger mandatory consumer notification.

The message from regulators is clear. Secure document sharing is no longer only a best practice, but it is a legal requirement with real consequences for non-compliance.

Core Security Principles for Financial Document Sharing

Effective document security rests on four pillars: confidentiality, integrity, accountability, and availability. Each pillar requires specific technical and procedural controls.

Confidentiality Through Encryption and Access Control

Encryption transforms readable documents into unreadable ciphertext that cannot be reversed without the decryption key. For financial documents, the standard is AES-256, the same encryption used by banks and government agencies to protect classified information. This standard applies to data at rest on your devices and servers, and to data in transit across networks using modern TLS protocols.

End-to-end encryption takes this further by ensuring documents are encrypted on your device before they ever reach a server. The service provider stores only ciphertext. They cannot read your files, even if compelled by legal order. This architecture, sometimes called zero-knowledge, significantly reduces the risk that a vendor breach or insider threat could expose client documents.

Access controls determine who can view, download, edit, or share documents. Role-based access control assigns permissions based on job function rather than individual file grants. A tax preparer sees only their assigned clients' returns. A reviewer sees only documents flagged for quality control. A partner sees firm-wide summaries but not every individual detail. This principle of least privilege limits the damage if any single account is compromised.

Multi-factor authentication adds another critical layer. Even if an attacker steals a password, they cannot access documents without the second factor, whether that is a code from an authenticator app, a hardware security key, or a biometric scan. The FTC now mandates MFA for all financial institutions under the amended Safeguards Rule, and cyber insurers increasingly deny claims when MFA was not implemented.

Integrity and Accountability Through Audit Trails

Knowing who did what, when, and from where is essential for both security and compliance. Detailed audit trails capture every action taken on a document: uploads, views, downloads, edits, permission changes, and deletions. Each entry includes the user identity, timestamp, IP address, device information, and the nature of the action.

These logs serve multiple purposes. They help detect unusual activity, such as a sudden spike in downloads from an unfamiliar location. They provide evidence for regulatory inquiries, demonstrating that your firm maintained reasonable control over client data. They support internal governance, enabling oversight and separation of duties. And they feed into incident response, helping identify the scope and timeline if a breach occurs.

For maximum protection, audit logs should be stored immutably, meaning they cannot be altered or deleted after creation. Cryptographic hashing can verify that logs have not been tampered with. WORM storage, which allows data to be written once and read many times but never modified, provides another layer of assurance.

Availability and Resilience

Security means nothing if authorized users cannot access documents when needed. The 3-2-1 backup rule remains the gold standard: maintain at least three copies of critical data, on two different media types, with one copy stored offsite or in a separate cloud region. Backups must themselves be encrypted and tested regularly. A backup that cannot be restored is a false promise, not a genuine safeguard.

Business continuity planning should explicitly cover document repositories and sharing workflows. If ransomware encrypts your primary systems, if a natural disaster damages your office, or if a vendor experiences an outage, you need documented procedures for restoring document access within timeframes that meet client and regulatory expectations.

Best Practices Across the Document Lifecycle

Secure sharing involves practices that span the entire document lifecycle, from creation to destruction.

Choose Purpose-Built Secure Platforms

Move away from email attachments and consumer cloud storage toward secure file-sharing platforms designed for sensitive documents. These platforms provide encryption, granular permissions, multi-factor authentication, access expiration, and detailed audit logging as core features rather than afterthoughts.

When evaluating platforms, prioritize technical security over marketing claims. Look for client-side or end-to-end encryption, transparent documentation of the encryption architecture, and evidence that the provider cannot access your unencrypted documents. A platform that publishes security whitepapers, invites vulnerability disclosure, and explains its key management in detail often demonstrates more confidence than one that relies solely on certification badges. Compliance certifications such as SOC 2 Type II or ISO 27001 can provide additional assurance, but they should supplement, not replace, verifiable technical controls. Also ensure the platform integrates with your existing practice management or document management systems, so secure sharing becomes the path of least resistance rather than an extra step.

Classify Documents by Sensitivity

Not every document requires the same level of protection. A public marketing brochure does not need encryption and expiration. A tax return containing Social Security numbers and bank account details does. Implement a simple classification framework: public, internal, confidential, and restricted. Map each level to specific controls. Highly sensitive documents should require end-to-end encryption, MFA, one-time download links, and short expiration windows. Less sensitive documents may tolerate broader access but should still be shared through secure channels rather than open email.

Set Expiration and Revocation by Default

Every shared document should have a defined lifespan. Configure your sharing platform to default to the shortest practical timeframe. A document needed for a single review should expire in 24 hours. A tax return shared with a client for signature might remain available for seven days. A loan file under active processing might need 30 days. You can always extend access if needed. It is far easier to grant additional time than to recover from an unauthorized disclosure.

Immediate revocation capability is equally important. If you send a document to the wrong recipient, if a client relationship ends, or if you suspect compromise, you must be able to deactivate access instantly with a single click.

Communicate Passwords Separately

When password protection is used, never send the password in the same email as the document link. Use SMS, phone calls, or secure messaging apps. This simple practice prevents a compromised email account from yielding both the document and the key to access it.

Encrypt Endpoints and Removable Media

The IRS Security Six mandates AES-256 full-disk encryption on all devices containing taxpayer data. This includes laptops, desktops, external drives, and USB devices. Use BitLocker for Windows, FileVault for macOS, or hardware-encrypted drives for removable media. Store recovery keys in secure locations with dual control access, not on the encrypted device itself.

Train Everyone

Technology alone cannot secure documents. Your staff must understand why secure sharing matters and how to do it correctly. Training should cover phishing recognition, proper use of secure links, recipient verification, password protocols, and incident reporting. Make training role-specific. Tax preparers need different guidance than receptionists. Update training quarterly, not annually, because threats evolve faster than yearly refresh cycles.

Document Your Practices

Regulators and insurers increasingly expect written evidence of security practices. Maintain documented policies covering approved sharing methods, prohibited practices, classification rules, retention schedules, and incident response procedures. Keep records of vendor assessments, training attendance, access reviews, and penetration test results. These documents are not bureaucratic exercises. They are your defense if a breach triggers regulatory inquiry or litigation.

Real-World Scenarios for Financial Professionals

Theory matters less than practice. Here are specific situations where secure document sharing transforms risk into control.

Sharing Tax Returns with Clients

During tax season, preparers send completed returns to clients for review and signature. Email attachments create permanent copies in client inboxes, on mail servers, and in backup systems. If the client's email is compromised, every tax return they have ever received is exposed.

A secure sharing platform eliminates this risk. The preparer uploads the encrypted return and shares a time-limited link. The client accesses the document through a password-protected portal, reviews it, and signs electronically. The link expires automatically after seven days. The preparer sees exactly when the client accessed the document. If the client needs more time, a new link is generated instantly. The original return remains secure in the preparer's encrypted repository, with access logged for compliance.

Transmitting Wire Instructions

Business email compromise schemes targeting wire transfers have cost businesses billions. Attackers intercept email threads, modify account numbers, and redirect funds. Bar associations and financial regulators explicitly advise against sending wire instructions via standard email.

Instead, host instructions in a secure platform and share through a time-limited, password-protected link that expires shortly after the recipient accesses it. Communicate the password by phone. Once the transfer is confirmed, revoke the link. Access logs provide a record that the correct recipient retrieved the correct instructions at a specific time, which can help resolve fraud disputes.

Exchanging Documents with Third-Party Verifiers

Mortgage applications require verification documents from employers, banks, and investment firms. These documents contain sensitive employment and financial data that must be shared with lenders and underwriters. Consumer cloud links or fax transmissions create uncontrolled copies.

A secure sharing platform allows each party to upload documents into an encrypted, access-controlled environment. The lender receives a link valid only for their review period. The employer's verification letter is accessible only to the loan officer handling that specific application. Audit trails document every access for compliance and dispute resolution.

Sharing Financial Plans with High-Net-Worth Clients

Wealth managers create detailed financial plans containing account details, estate information, business ownership structures, and family financial data. These documents are targets for sophisticated attackers seeking to exploit high-value individuals.

Secure sharing with device binding, IP restrictions, and dynamic watermarks provides multiple layers of protection. The client accesses the plan from their known home or office network. The document displays their email address as a visible watermark, deterring casual forwarding. The link expires after the review meeting. If the client needs to share with their attorney or accountant, separate links with independent controls are created for each party.

FAQ: Common Questions About Secure Financial Document Sharing

Is email ever acceptable for sharing financial documents?

For routine, non-sensitive communications such as scheduling or general inquiries, standard email is generally acceptable. For documents containing Social Security numbers, account details, tax information, or any regulated financial data, email attachments should be avoided. Use secure file-sharing platforms with encryption, access controls, and audit trails instead.

What encryption standard should I look for?

AES-256 is the current gold standard for encrypting financial documents. It is approved by NIST for protecting top-secret information and is widely regarded as computationally infeasible to break. Ensure encryption applies both to data at rest on servers and devices, and to data in transit across networks using modern TLS protocols.

Does the IRS require specific sharing methods for tax documents?

The IRS does not mandate specific technologies, but the Security Six framework and Publication 4557 require that tax professionals implement encryption, access controls, audit trails, and secure disposal for all systems containing taxpayer data. Email attachments and consumer cloud links that lack these controls do not meet the standard.

What is the difference between client-side and server-side encryption?

With server-side encryption, your file is uploaded to the provider in plaintext, and the provider encrypts it on their servers. They hold the keys and can decrypt your data. With client-side encryption, your file is encrypted on your device before upload. The provider stores only ciphertext and cannot read your documents. Client-side encryption provides stronger protection against provider breaches.

How long should I retain shared financial documents?

Retention periods vary by document type and jurisdiction. Tax records are generally retained for three to seven years. Broker-dealer records often require six years under FINRA rules. The GLBA Safeguards Rule requires secure disposal of customer information no later than two years after last use, unless required by law. Your written security plan should specify retention periods for each category.

What should I do if I suspect a document was shared inappropriately?

If shared through a secure platform, revoke the link immediately and review access logs to determine who accessed the document. Document your response actions. Notify your firm's security coordinator. If the document contained regulated data, consult your incident response plan and consider whether breach notification obligations apply. Report suspected data theft to the IRS and relevant authorities as required.

Are secure sharing platforms difficult for clients to use?

Modern platforms are designed for simplicity. Clients receive a link, click it, enter a password or verification code if required, and view or download the document. The encryption and security controls operate invisibly in the background. No software installation, no technical expertise, no friction. The experience is often simpler than downloading an email attachment and navigating password-protected ZIP files.

What should I look for when choosing a secure document sharing platform?

Prioritize client-side or end-to-end encryption with AES-256. Verify multi-factor authentication. Confirm granular access controls. Look for detailed audit trails with immutable log storage. Ensure configurable link expiration and instant revocation. Review the provider's security documentation. A platform that explains its encryption architecture in detail often demonstrates more confidence than one relying solely on certification badges.

Conclusion: Security Is a Professional Responsibility

Financial professionals occupy a unique position of trust. Clients hand over their most sensitive information, Social Security numbers, bank accounts, income details, family financial data, with the expectation that it will be protected with the same care as the advice itself. That trust is increasingly codified in law, not merely an ethical ideal.

The IRS Security Six, the GLBA Safeguards Rule, state breach notification laws, and cyber insurance requirements have converged on a single message: secure document sharing is a professional obligation, not a technical preference. Email attachments and consumer cloud links no longer meet the standard. Regulators expect encryption, access controls, audit trails, and secure disposal. Clients expect their information to be handled with modern safeguards. And attackers are betting that many professionals have not yet made the shift.

The tools to meet these expectations are now accessible to practices of every size. Secure file-sharing platforms make bank-grade encryption, time-limited access, and detailed audit trails as easy to use as sending an email. The technology handles the complexity. You handle the decision to use it.

Your clients trust you with their financial lives. That trust deserves better than an attachment that lives forever in someone else's inbox.

Ready to protect your financial documents with bank-grade encryption, self-destructing links, and complete access control? Create your first secure file sharing link with SecureSend and experience effortless, ultra-secure document sharing built for financial professionals in 2026.

Sources: IBM Cost of Data Breach Report 2025, Identity Theft Resource Center 2025 Annual Data Breach Report, IRS Publication 4557, FTC Safeguards Rule (16 CFR Part 314), FBI Internet Crime Complaint Center 2026, Secureframe Data Breach Statistics 2025.